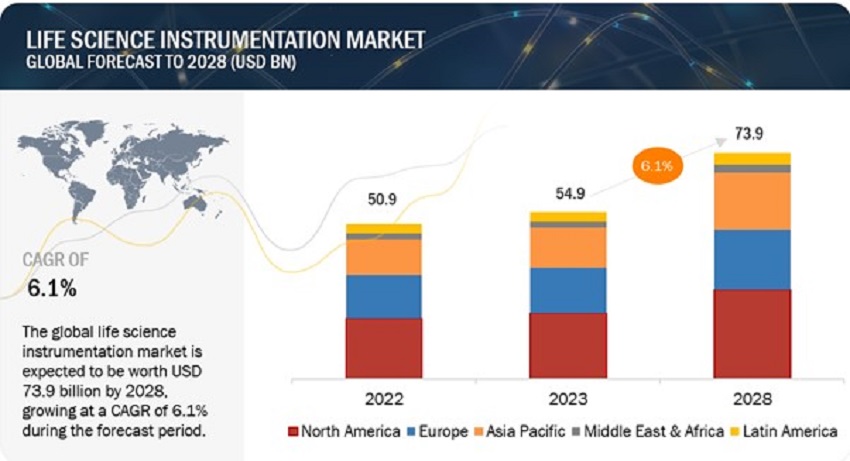

The global life science instrumentation market is experiencing robust growth, with a projected worth of $73.9 billion by 2028, according to a report published in 2023. This impressive growth, at a CAGR of 6.1% from 2023 to 2028, is attributed to several key factors driving the market's expansion.

Download PDF Brochure-https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38

One of the primary drivers of this growth is the increasing number of research grants and investments in pharmaceutical research and development (R&D). The pharmaceutical industry, in particular, is focusing on manufacturing protein-related products, necessitating a wide range of analytical instruments for tasks such as drug molecule evaluation, protein analysis and purification, and quality control. This trend has been further accelerated by significant foreign direct investments and government funding in pharmaceutical R&D, particularly in emerging markets.

However, the market is not without its challenges. High equipment costs pose a significant restraint, driven by recent technological advancements and the addition of features such as automation with AI integration. While these advanced instruments offer accuracy and efficiency, they are often expensive to acquire and maintain. This cost factor has limited their adoption by small-scale users, including academic and research institutions and smaller pharma-biopharma companies, who often operate with tight budgets.

Despite these challenges, opportunities abound in the life science instrumentation market, notably in the widening application scope of analytical instruments. These instruments find applications in diverse sectors, including food and beverage, environmental testing, and forensics. Analytical techniques are crucial for quality control in food production, detecting contaminants, and ensuring the safety of packaging materials. In environmental testing, these instruments help analyze air and water samples, detecting pollutants and trace gases. With an increasing focus on environmental conservation, the demand for life science instruments in these application segments is on the rise.

Nonetheless, inadequate research infrastructure in emerging countries remains a significant challenge. Emerging nations in Asia, the Middle East, and Africa often lack the necessary infrastructure, including financial support, well-equipped research laboratories, and trained professionals. This deficiency hampers the growth of the life science instrumentation market in these regions.

In terms of technology, spectroscopy emerged as the dominant segment in 2022, driven by its extensive use in oncology research and the need for improved sensitivity and speed.

Pharmaceutical and biotechnology companies represented the largest end-user segment in 2022, given the substantial utilization of life science equipment in medication development and research and development activities.

Looking at applications, the research segment is expected to witness significant growth in the near future, fueled by available funding for R&D activities in academic institutions.

Geographically, North America, led by the United States and Canada, held the largest market share in 2022. Factors contributing to this include increased research funding, a growing healthcare/medical sector, and the presence of major industry players in the region.

Some prominent players operating in the global life science instrumentation market include Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Waters Corporation (US), and Shimadzu Corporation (Japan).

Download PDF Brochure-https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38

As the life science instrumentation market continues to evolve, driven by a combination of factors including increasing R&D investments and widening application horizons, it is poised for substantial growth in the coming years, offering new opportunities for both established companies and emerging players in the industry.